The world confronts the weakest medium-term growth outlook in three decades amid high debt levels, fragmented trade, and the prospect of higher-for-longer interest rates. In this environment, the IMF is redoubling its efforts to promote stability and growth.

All countries grapple with uncertainty from shocks related to the pandemic, war in Ukraine, and transformational challenges such as climate change and digitalization. Several emerging market and developing countries have shown remarkable resilience. But many—especially low-income countries—are increasingly vulnerable amid tighter financial conditions, limited policy room for maneuver, and dwindling buffers.

These countries also face a funding squeeze, heightened food insecurity, and a slower convergence toward higher living standards. High debt burdens and a sharp increase in debt servicing costs—exceeding 40 percent of revenues in several highly indebted countries—leave little space for social spending and growth-enhancing investment. This adversely impacts debt sustainability and social stability.

The IMF is responding to calls to play an even greater role to support our member countries during these very challenging times, importantly through the provision of balance of payments financing and policy advice.

Crises and channeling

To be sure, the Fund acted to help members address balance-of-payments needs from recent shocks. This includes providing emergency financing and temporarily increasing access limits for Fund arrangements. We approved precautionary financing arrangements and established a Short-term Liquidity Line that serves as a backstop for members with very strong fundamentals. We responded to the global food crisis stemming from Russia’s war in Ukraine by introducing a Food Shock Window in September 2022 to help countries facing urgent balance of payments needs related to food insecurity.

Since the pandemic, we have deployed $1 trillion in global liquidity and reserves through our lending and the 2021 allocation of $650 billion in special drawing rights, or SDRs. We have provided around $320 billion in financing to 96 countries. We have increased five-fold our interest-free financing to 56 low-income countries through our Poverty Reduction and Growth Trust. And we have worked with economically stronger members to channel a significant share of their SDRs to more vulnerable countries, generating around $100 billion in new financing through IMF trusts such as the PRGT and the Resilience and Sustainability Trust introduced last year.

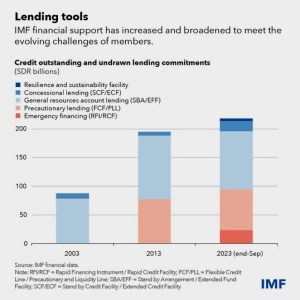

As a result, the IMF has committed unprecedented financial resources to members. As of September, the IMF has lending commitments with 94 countries for about $287 billion, or SDR 218 billion. This includes:

- Precautionary facilities for seven emerging market economies for $93 billion

- Lending commitments for 35 emerging market economies for $134 billion

- Interest-free lending of $23.5 billion for 45 low-income countries

- $30.5 billion of outstanding credit on emergency financing for 77 countries

- Long-term loans of about $6 billion to 11 emerging market economies under the RST’s Resilience and Sustainability Facility. Around 40 more countries have requested or expressed interest in an RSF arrangement.

We continuously assess and improve our lending toolkit to ensure that can address today’s and tomorrow’s challenges:

- Since preventing crises is far less costly than resolving them, we recently reviewed our precautionary instruments—the Flexible Credit Line, the Short-Term Liquidity Line and the Precautionary and Liquidity Line. Reforms seek to improve their agility and capacity and ensure their strong signaling power. Access limits increased for some instruments. Concurrent use will allow users to address different balance-of-payments needs. For the first time, users will not need to articulate a strategy for exit from relatively lower levels of access of the Flexible Credit Line.

- We also reformed the non-financial Policy Coordination Instrument. This instrument enables countries to signal the quality of their policies, which helps catalyze external financial support from official and private sources. Reforms improve the flexibility and signaling power of the instrument.

- Work on helping countries in or near debt distress continues, and additional debt policy reforms are under consideration. This includes creditor cooperation and financing assurances, supporting better engagement with the member and creditors, and supporting members undergoing debt restructurings when they face extraordinary circumstances. The IMF also co-chairs the Global Sovereign Debt Roundtable to bring borrowing countries together with both official and non-official creditors.

- Our forthcoming reviews of our conditionality and recommendations of our Independent Evaluation Office on exceptional access will help us strengthen our support to members. They will also ensure that Fund financing continues to help unlock other funding sources elsewhere.

Looking ahead

The IMF is committed to continue supporting member countries through policy advice, capacity development, and lending. The challenge is to support vulnerable countries that have limited fiscal space to implement politically costly reforms. Yet when financing is front-loaded but adjustment and reforms are backloaded, credibility is harder to establish. Securing additional external financing becomes difficult. All this puts at risk the completion of program reviews and the achievement of macroeconomic stabilization.

To help countries undertake and sustain adjustment, reforms and financing are needed that pay off sooner in terms of growth. Where debt concerns are acute, debt restructuring, and more grant financing may also be needed. The Fund is deepening collaboration with the World Bank and other multilateral institutions with expertise in structural reform areas, to suitably calibrate and sequence reforms under their core areas of work.

We need to ensure that the IMF has the resources to effectively exercise its lending function. The successful completion of the ongoing 16th General Review of Quotas will be essential to secure the Fund’s general resources, together with closing remaining fundraising gaps for the PRGT and RST. These will ensure that lending to vulnerable countries can continue in adequate volume and on favorable terms.

IMF Blog