An emergency 50 billion Swiss Franc loan from the Swiss National Bank in the early hours of Thursday helped to pull one of Switzerland’s top banking institutions, Zurich-based Credit Suisse, from the brink of collapse.

At first sight, the move proved a regulatory tour de force.

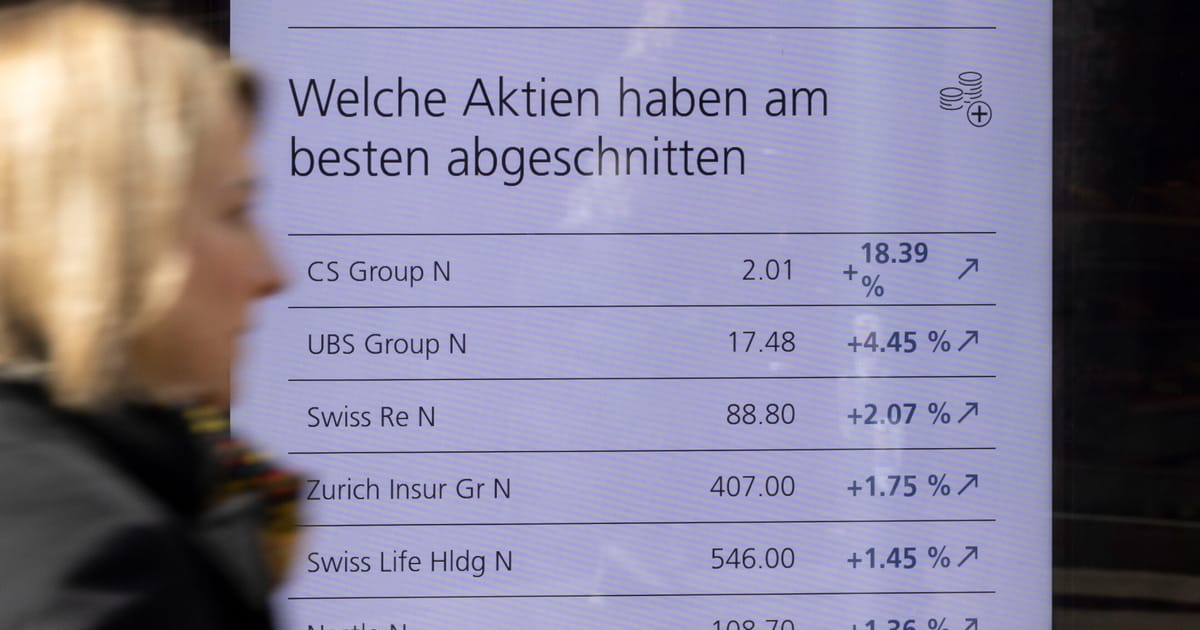

When the bank’s shares opened for trading in the morning, they soared 40 percent, an apparent nod to the shrewdness of Eurocrats who had been saying all along this was not Europe’s crisis and that there was nothing to see here.

From a regulatory point of view, the troubles at the Swiss lender had been brewing for years and had little to do with the factors that had taken down Californian tech lender Silicon Valley Bank a week earlier, prompting a radical Federal Reserve intervention at the weekend.

What’s more, Credit Suisse had long been in the process of restructuring, dragged down by a series of unfortunate bets and scandals.

The defiant regulatory mood was echoed by Christine Lagarde, president of the European Central Bank, at Thursday’s interest rate policy meeting. While markets had been braying for a break to her intensive rate-hiking schedule, Lagarde stayed her course. The European banking system could handle it, she signaled.

What markets wanted to know was … would she go on to regret it?

The reaction in equity markets was telling. The share prices of major European banks, among them Germany’s Deutsche Bank and France’s Société Générale, continued their downward trajectory following the meeting, with even Credit Suisse paring back earlier gains.

Mistakes being repeated?

Over a decade earlier, one of Lagarde’s predecessors, Jean-Claude Trichet, had stubbornly continued to raise rates into what became the 2011 sovereign debt crisis. The stress pushed many parts of peripheral Europe to the edge of economic collapse and rocked market faith in the single monetary euro system.

Today, analysts are still divided on whether Lagarde is making the same mistake again.

“Trichet hiked into a selloff in peripheral sovereigns that price off of ECB rates,” said Elettra Ardissino, senior Europe analyst at Greenmantle. “There’s little evidence that the banking panic is spreading to sovereigns — BTP-Bund [the difference between the cost of Italian and German debt] spreads are still contained.”

Others, such as Marc Ostwald of ADM Investor Services, believe the risk lies elsewhere, potentially in core European countries like Germany, many of which are facing the double whammy of growing public deficits and debt ratios on the back of pandemic spending and the impact of Ukrainian support measures, as well as the sharpest turnaround in the cost of their financing, having previously benefited from zero or negative rates.

“Markets are a confidence game, and confidence is in very scarce supply,” Ostwald told POLITICO. “There are numerous risks: widening eurozone government spreads, the return of Japan risk premium and there’s still a risk of U.S. debt ceiling drama.”

The Swiss National Bank’s move to backstop Credit Suisse may have echoed what Lagarde’s direct predecessor Mario Draghi had done when he announced the ECB was prepared to do “whatever it takes” to defend the system — but the dynamics of the public balance sheets of 2023 were likely to introduce new limitations.

Putting the full weight of a national economy behind a European bank might not be enough this time round.

For one thing, the impact of high interest rates on central bank balance sheets means even the strongest institutions, such as the Swiss National Bank, are already registering losses, beckoning the possibility that governments will have to infuse them with taxpayer funds.

Central bankers rebut such concerns, saying that even if governments withhold support from their institutions, they can never go bust because they have access to their own money printers.

But such defenses only make sense in the context of inflation being tamed, economic well-being improving and trust in the sovereign currencies remaining high. Without those three fundamentals present, the pathway to becoming a new Argentina cannot be ruled out.