Think about you’re the boss of a financial institution financed solely by debt and subsequent to no fairness. A lot of this debt serves as the cash utilized by the general public to pay their payments, whereas the financial institution’s belongings are each illiquid and dangerous. This, you would possibly assert, is a fairy story: no one would lend to such a enterprise. However suppose lenders have been positive these money owed have been assured by taxpayers. It will then grow to be a money-making machine: all upside; no draw back.

Once more, you may think that no governments would make such a dedication. Formally, after all, their ensures are restricted to smaller deposits. However there can nonetheless be implicit ensures, as a result of governments don’t want banks to break down in a panic.

Once more, one would count on governments to make sure that banks don’t get such ensures for nothing: they’d insist on substantial risk-bearing fairness and huge holdings of protected liquid belongings.

Earlier than the worldwide monetary disaster, there have been certainly some such necessities. However they have been ineffective. For a lot of important establishments the ratio of fairness to complete belongings was just some 2 per cent.

How did this occur? Banks have been allowed to mark their very own homework by “risk-weighting” their belongings. On this manner the “risk-weighted capital ratio” may very well be magically elevated. These weights have been drawn from expertise. In 2006, this urged that dangers had by no means been smaller. Banks have been deemed exceptionally protected simply as they turned exceptionally unsafe. That’s what occurs in credit score gluts.

Thereupon a collection of “surprises”, notably the falling home costs, destabilised the system. The solvency and liquidity dangers have been certainly socialised. The assumption that states assured the banking system proved appropriate.

Permitting a lot of the banking sector to function with close to zero fairness and an upside-only contract for bankers was mad. It occurred partly due to the assumption that “it’s completely different this time”. Additionally, nearly all people loves a credit score growth. However, within the case of the UK, there was one thing else: the assumption that banking is a revenue centre for the financial system. And so, it was concluded, the nation’s finance should be stored “aggressive” by “light-touch” regulation.

We might by no means let finance go rogue like that once more, one would possibly hope. However it’s now some 15 years because the disaster and, within the UK specifically, the federal government is determined for progress and funding.

I’m hardly shocked then that the brand new metropolis minister, Andrew Griffith, has harassed a brand new obligation on regulators to “facilitate progress and competitiveness”. The latter concept additionally permeates the Monetary Providers and Markets invoice now going by means of parliament. In any case, “alternatives of Brexit” are certain to incorporate extra permissive regulation.

Thus far, the steps are modest. That is additionally true of just lately urged modifications to the “ringfencing” regime launched after the 2011 report of the Impartial Fee on Banking (of which I used to be a member). However a journey of a thousand miles begins with a single step.

Ringfencing pressured banks to create a individually capitalised retail subsidiary. The goals are to isolate banking actions, the place steady provision of service is significant to the financial system and clients, facilitate decision of failing banks, and so get rid of implicit ensures to funding banking actions, which UK regulators can hardly monitor and are of no evident worth to the UK public.

This logic nonetheless applies. Bear in mind too that, pre-crisis, the stability sheets of UK banks have been 5 occasions GDP, a lot of this consisting of world actions. Banks have been too large to fail, however, for the UK, nearly too large to save lots of. Ringfencing helps restrict these dangers. Encouragingly, Financial institution of England analysis even finds a “ringfence bonus”: it “is perceived by third events as insulating the ringfenced financial institution subsidiary from threat”. But “there is no such thing as a important influence on the perceived riskiness of the non-ringfenced financial institution”.

Ringfencing was partly justified by what we thought-about excessively low necessities for fairness. Is that this concern now outmoded? Completely not.

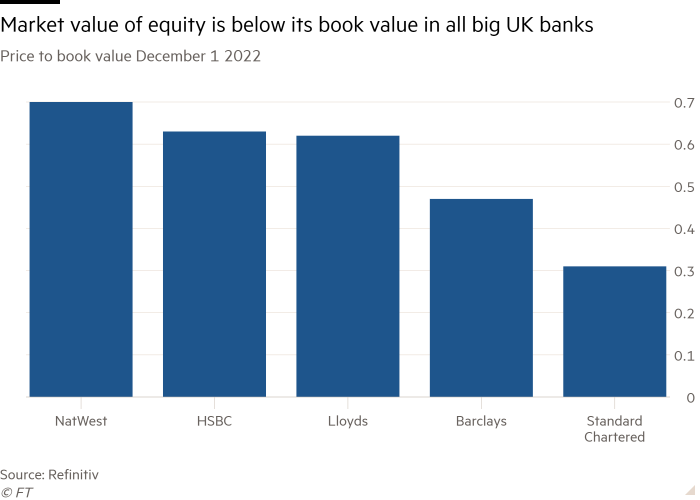

Sure, there’s extra fairness in banks now, however not that rather more. The ratio of fairness to belongings in UK banks within the first quarter of this 12 months was solely 5.3 per cent. That is known as a relatively small cushion. Worse, these ratios replicate the values in banking books. Markets worth financial institution belongings at beneath their guide worth within the UK (and in all places else, besides North America). This means that traders doubt the standard of the belongings and so of financial institution fairness. This can be a disturbing sign.

We should not chill out the ringfence, not least as a result of UK banks stay undercapitalised. Extra broadly, the thought of selling competitiveness by enjoyable regulation is perilous. The dangers will emerge slowly: Sunak and the remainder of his authorities shall be lengthy gone. However the mantra of “competitiveness” will begin the journey down a dangerously slippery slope. We should be cautious: banks constructed on upside-only bets for his or her determination makers are positive to crash.

martin.wolf@worldnewsintel.com

Observe Martin Wolf with worldnewsintel and on Twitter