President Joe Biden and the Republican-controlled House of Representatives appear to be on a collision course over raising the statutory limit on the national debt. House Republicans say they want Biden to accept significant (but unspecified) spending cuts in exchange for raising the limit. But the president has insisted that raising the limit – which allows the government to continue paying its obligations under the law on time – shouldn’t be a budgetary bargaining chip.

Public concern about federal spending is on the rise. In a new Pew Research Center survey about the public’s policy priorities, 57% of Americans cited reducing the budget deficit as a top priority for the president and Congress to address this year, up from 45% a year ago. Concern has risen among members of both parties, although Republicans and Republican-leaning independents are still far more likely than Democrats and Democratic leaners (71% vs. 44%) to view cutting the deficit as a leading priority. (When the government spends more than it takes in, it borrows to make up the difference. The debt, therefore, can be seen as the accumulated sum of previous years’ deficits that is still outstanding.)

Federal borrowing has essentially already hit the current debt limit of $31.38 trillion, though Treasury Secretary Janet Yellen has said she can use a variety of accounting maneuvers to postpone a government default for a few months. So far, neither the administration nor the House is budging from the positions they’ve staked out, so the standoff continues.

With that in mind, here’s a primer on the national debt of the United States. (For more on the statutory debt limit, read “Why does the U.S. have a debt limit, anyway?” below.)

Why does the U.S. have a debt limit, anyway?

Aside from Denmark, the United States is the only country with a law setting a specific monetary limit on its national debt. (Australia enacted such a limit during the 2007-09 global financial crisis, only to repeal it a few years later.)

Some other countries have debt caps linked to their gross domestic product, meaning that as their economies grow the monetary value of the debt limit rises as well. European Union member countries, for example, are supposed to keep their public debts to no more than 60% of GDP, though in practice many countries are well in excess of that limit and enforcement has been inconsistent. (The EU limit was suspended during the COVID-19 pandemic but is due to return later this year.) And a handful of other countries, including Kenya and Malaysia, have laws limiting their public debt to a percentage of GDP, though those limits seldom generate the kind of recurring political battles that the U.S. debt limit does.

The U.S. has had public debt for longer than it’s been a country, but it managed to get along without a debt limit for more than a century and a half. The standard practice was for Congress to authorize specific debt issues for specific purposes – $11.25 million to fund the Louisiana Purchase, $500 million to wage the Civil War, $130 million to build the Panama Canal, and so forth. Along with the size of the bond issue, Congress might also specify the bonds’ denominations, interest rates, maturity dates, early redemption rules, and other terms and conditions.

But when the U.S. entered World War I in 1917, it was confronted with the need to borrow unprecedented sums of money. By the time the Treaty of Versailles formally ended the war in 1919, the U.S. had sold $21.5 billion in bonds, along with $3.45 billion in short-term certificates, with varying lengths, interest rates, redemption rules and tax treatments. Administering and paying down that debt proved to be too complex for Congress to micromanage.

The laws authorizing the World War I bonds – primarily what became known as the Second Liberty Bond Act – originally spelled out in some detail the terms and conditions of each bond issue. But throughout the 1920s and 1930s, as the various bond issues approached maturity and had to be either paid off or refinanced, Congress gave the Treasury Secretary more and more discretion to issue new and different types of debt securities – short-, medium- and long-term – under terms the secretary thought best.

Gradually, the specifications in the Second Liberty Bond Act (which in amended form came to govern most government borrowing) were replaced by broad caps. In 1939, the few remaining limits were replaced by an overall $45 billion cap that covered nearly all public debt – the birth of the statutory debt limit as we know it today.

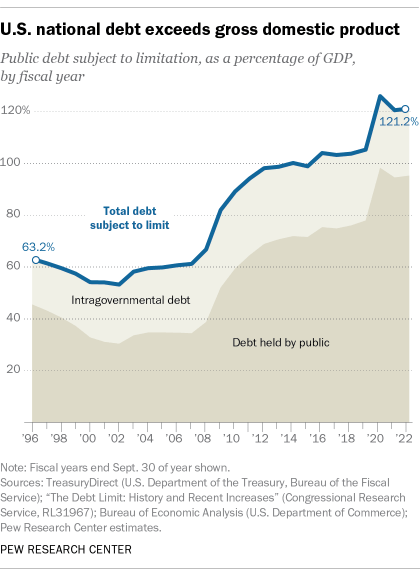

The federal government’s total public debt stood at just under $31.46 trillion as of Feb. 10, according to the Treasury Department’s latest daily reckoning. Nearly all of that debt – about $31.38 trillion – is subject to the statutory debt limit, leaving just $25 million in unused borrowing capacity.

For several years, the nation’s debt has been bigger than its gross domestic product, which was $26.13 trillion in the fourth quarter of 2022. Debt-to-GDP is a useful metric for analyzing the debt over long time spans, as it puts the debt into relative terms by comparing it against the size of the national economy. Looked at this way, debt as a share of GDP has gone through three main growth phases in recent decades. These have corresponded with periods when the federal government ran large budget deficits: the Reagan-Bush years of the 1980s and early 1990s; the 2008 financial crisis and subsequent Great Recession; and the pandemic-caused recession of 2020, when federal debt spiked to an all-time high of 134.8% of GDP. The ratio has come down a bit since but remains well above pre-pandemic levels.

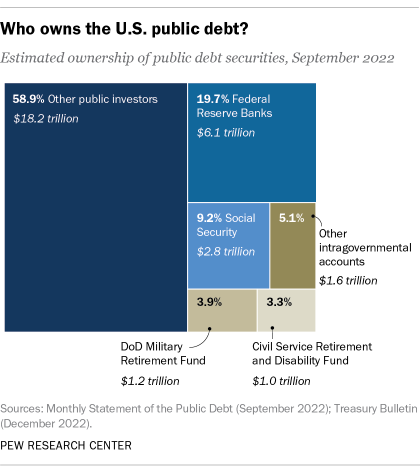

While U.S. government debt is perhaps the most widely held class of security in the world, 21.8% of the public debt, or $6.87 trillion, is owned by another arm of the federal government itself. That includes Medicare; specialized trust funds, such as those for highways and bank deposit insurance; and civil service and military retirement programs. But the biggest chunk of those “intragovernmental holdings” belongs to Social Security. As of the end of January, the program’s retirement and disability trust funds together held more than $2.8 trillion in special non-traded Treasury securities, or 9% of the total debt. (For many years, Social Security collected more in payroll taxes than it paid out in benefits; the surplus was required by law to be invested in Treasuries. That made Social Security, for a time, the federal government’s single biggest creditor.)

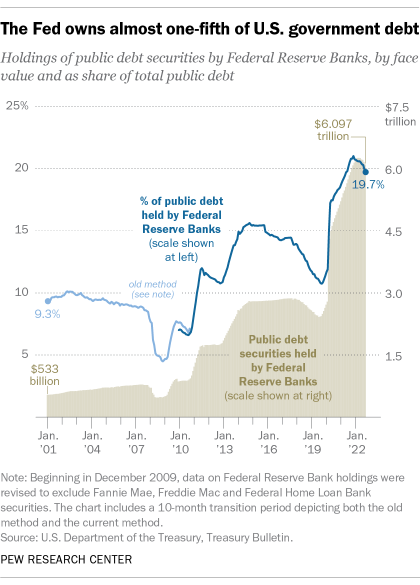

Today, the Federal Reserve System is the single largest holder of U.S. government debt. While the Fed regularly buys and sells Treasury securities to execute monetary policy, it bought Treasuries in massive quantities during the COVID-19 pandemic in an effort to keep the U.S. economy from buckling under the strain of shutdowns and quarantines.

At its peak in April 2022, the Fed held more than $6.25 trillion in U.S. government debt, more than double its holdings just before the pandemic hit the U.S. in March 2020. Even as the Fed has begun to scale back its holdings, it held nearly $6.1 trillion in government bonds – almost a fifth of the entire public debt – as of Sept. 30, 2022, the most recent data available. A decade earlier, by contrast, the Fed’s share of the debt was just under 11%. (Because the Fed is formally independent of the federal government, its stash isn’t included among the intragovernmental holdings discussed above.)

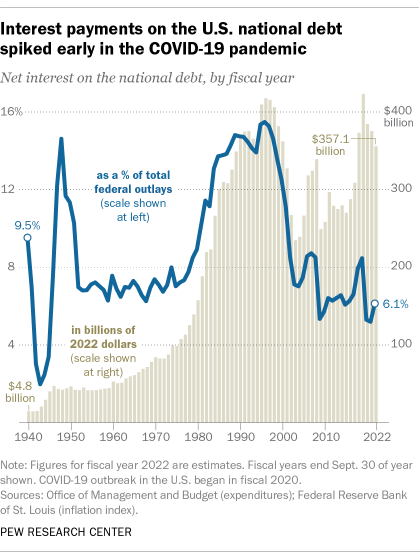

Servicing the debt is one of the federal government’s biggest expenses. Net interest payments on the debt are estimated to total $395.5 billion this fiscal year, or 6.8% of all federal outlays, according to the Office of Management and Budget. That’s more than $100 billion more than the government expects to spend on veterans’ benefits and services and more than it will spend on elementary and secondary education, disaster relief, agriculture, science and space programs, foreign aid, and natural resources and environmental protection combined.

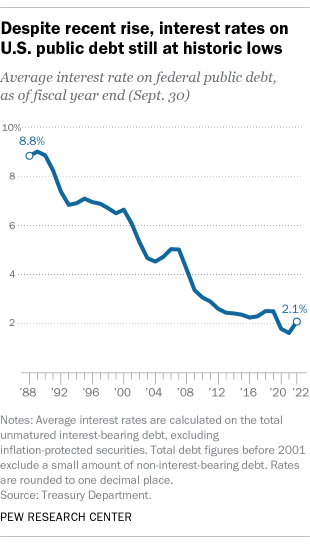

Debt service as a share of federal outlays peaked at more than 15% in the mid-1990s, but generally falling interest rates have helped hold down payments even as the dollar amount continues to grow. In fiscal 2021, the average interest rate on federal debt was a record-low 1.605%. But with the Fed raising its policy rate to try to cool off the economy, the U.S. has started paying more to borrow: The average interest rate on federal debt last year ticked up to 2.07%.

Note: This is an update to a post originally published on Oct. 9, 2013.